401k Calculator: Best Free Retirement Savings Estimator

A 401 (k) calculator is the most important tool you can use before planning your retirement. Without a 401 (k) calculator, you are just guessing. This 401 (k) calculator helps you see exactly how much your savings will grow based on your salary, contribution rate, and employer match.

Planning for retirement is one of the things you can do with your money. Most people have no idea how much they will actually have when they stop working. A 401k calculator helps you figure out how much you will have. It shows you in numbers how your contributions today will grow into real wealth tomorrow.

Whether you are 25 and just starting or 50 and playing catch-up, this guide walks you through how a 401 (k) calculator works. We will look at what inputs matter and how to use them to build the retirement you deserve.

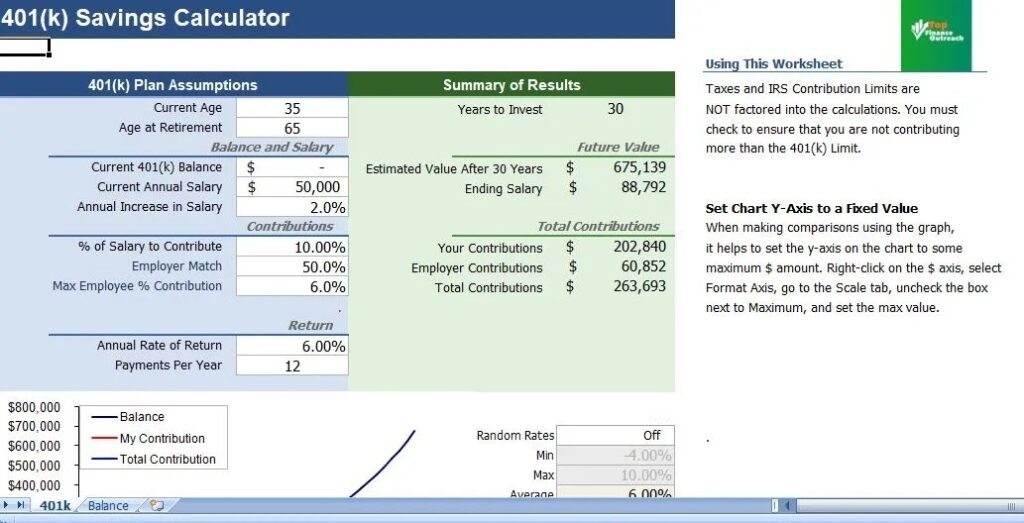

401(k) Calculator

Estimate your balance at retirement based on your contributions and employer match.

What Is a 401k Calculator? Why Does It Matter?

A 401k calculator is a tool that projects the future value of your retirement account. You control the variables: your salary, contribution rate, employer match, investment return, and expected retirement age. A 401k calculator is a tool that projects the future value of your retirement account. You control the inputs: salary, contribution rate, employer match, investment returns, and retirement age.

A 401(k) is a tax-advantaged retirement savings plan offered by employers in the United States. To understand the full rules, contribution limits, and withdrawal policies, you can read the complete guide to 401(k) plans..

A 401k calculator works by taking your inputs and applying compound interest over time. Every time you use a 401 (k) calculator, you get a clearer picture of your retirement future. Think of a

401 (k) calculator as your personal retirement GPS.

Think of it like a GPS for your retirement. You enter where you are today and where you want to go. It maps the route. Without it, you are driving blind. Most Americans underestimate how much they will need in retirement. According to data, nearly half of working-age adults have nothing saved.

A 401k estimator forces you to confront that reality. Then fix it.

How Does A 401 (k) Calculator Work?

A good 401k calculator with match functionality uses a compounding formula. Here is what it calculates step by step:

Step 1: Your Annual Contribution: You enter your salary and the percentage you plan to contribute. For example, if you earn $70,000 and contribute 6%, that is $4,200 per year going into your account.

Step 2: Your Employer Match: Most employers match a portion of your contribution. The common structure is 50% match up to 6% of your salary. In the example, your employer would add another $2,100. At zero cost to you. Over 30 years, that free money compounds into tens of thousands of dollars.

Step 3: Investment Growth: Your money does not sit still. It grows. A typical term average return assumption is 6–7% annually, accounting for market fluctuations. The calculator applies compound interest year over year, which’s where the real magic happens.

Step 4: Your Projected Balance: Finally, the calculator outputs your estimated 401 (k) balance at retirement. You can adjust variables in time to see exactly how contributing 1% more. Or starting 5 years earlier. Changes your outcome.

2025 & 2026 IRS 401 (k) Contribution Limits:

Before running your numbers, know your limits. The IRS adjusts 401k contribution caps for inflation. Here are the current figures:

| Contribution Type | 2025 Limit | 2026 Limit |

| Employee Contribution | $23,500 | $24,500 |

| Catch-Up (Age 50–59, 64+) | +$7,500 | +$8,000 |

| Super Catch-Up (Age 60–63) | +$11,250 | +$11,250 |

| Total (Employee + Employer) | $70,000 | $72,000 |

These limits apply to US-based 401 (k) plans. If you are in Canada, the UK, or another country, equivalent plans (RRSP, workplace pension) have their own contribution rules. The 401 (k) calculator logic, however, applies universally to any tax-qualified retirement account.

401k Calculator With Match: Why The Employer Match Changes Everything

The employer match is the most underutilized benefit in personal finance. It is literally free money. And millions of workers leave it on the table every year.

Here is a real-world example:

- salary: $60,000

- Your contribution: 6% = $3,600/year

- Employer match: 50% up to 6% = $1,800/year

- Total going into your account: $5,400/year

- Over 30 years at 7% return: approximately $544,000

Now cut your contribution to 3%: you miss $1,800 in employer money every single year. Over 30 years, that missed match. Compounded. Costs you over $180,000 in lost retirement savings.

A good 401k calculator with a match shows you this gap instantly. Always contribute enough to capture your full employer match. It is a 50–100% return on your investment. Many people struggle financially in retirement because they don’t plan early. Strong financial habits matter more than income alone.

401k Growth Calculator: The Power Of Starting

Time is your most powerful asset in retirement savings. The earlier you start, the less you actually have to contribute. Because compounding does the lifting.

Consider two workers, both targeting $1 million at age 65:

- Sara starts at 25 and contributes $300/month. Reaches $1M+ comfortably

- James starts at 40, contributes $300/month. Reaches ~$340,000

- James would need to contribute ~$880/month to match Sara

A 401k growth calculator makes this visible. Use it to experiment with start ages and see the cost of waiting. It is one of the most motivating exercises you can do for your financial future.

Common Mistakes To Avoid When Using a 401 (k) Calculator

A calculator is only as good as the inputs you give it. Watch out for these errors:

1. Using an Unrealistic Return Rate: Many people plug in 10–12% returns, which are optimistic. A conservative and realistic figure is 6–7%, accounting for fees and market volatility. Overestimating returns leads to under-saving.

2. Forgetting Inflation: A million dollars today will buy less in 30 years. Some calculators include an inflation adjustment. Use it. A 3% inflation rate is an assumption for long-term planning.

3. Ignoring Vesting Schedules: Your employer match may not be yours right away. Many companies use a 3–4 year graded vesting schedule. If you leave before vesting, you forfeit a portion of those employer contributions. Always check your plan documents.

4. Not Updating Your Projections Annually: Life changes. So should your 401 (k) estimator inputs. A salary raise, a job change, or a new employer match policy can significantly shift your retirement trajectory. Revisit your projections every year.

How To Read Your 401 (k) Calculator Results

Once you run the numbers, your calculator will typically show:

- Estimated balance at retirement. Your projected total

- Total contributions. How much you personally put in

- Total employer contributions. The money you earned

- Total investment growth. The compounding magic

Together, these four numbers tell the full story of your retirement. In projections, investment growth is the largest component. Often, 50–60% of your final balance. That is why staying invested matters more than trying to time the market.

Your 401 (k) is just one part of retirement planning. Many investors also explore passive income strategies to build wealth faster.

Expert Perspective: What Financial Planners Look For

Certified financial planners consistently emphasize three benchmarks when evaluating a 401k plan:

- Save at least 15% of your income for retirement (including employer match)

- Aim for a balance to 1x your salary by age 30 3x by 40 6x by 50 8x by 60

- Maximize employer match before contributing to any other account

These are not rules. They are starting benchmarks. Your actual target depends on your lifestyle, expected Social Security income, other assets, and planned retirement age. A 401k calculator gives you the number behind these general guidelines. Retirement planning is part of a larger financial ecosystem. Technology and markets are also changing how people invest and save.

Asked Questions (FAQs)

What is a 401 (k) calculator used for?

A 401 (k) calculator helps you estimate how much money you will have saved by the time you retire. It accounts for your salary, contribution rate, employer match, investment returns, and years until retirement to project your balance.

How accurate is a 401 (k) growth calculator?

It is a projection tool, not a guarantee. The accuracy depends on your inputs. The assumed rate of return. Most financial advisors recommend using a 6–7% return rate for more reliable long-term estimates.

What is a good contribution rate for a 401k?

At a minimum, contribute enough to capture your employer’s match. Beyond that, most financial planners recommend saving a total of 10–15% of your income (employee + employer combined) for retirement.

Can people outside the US use a 401 (k) calculator?

Yes. The underlying math applies to any retirement savings account. If you are in Canada (RRSP), the UK (workplace pension), or another country, you can use the compound interest logic. Just substitute your contribution limits and employer match terms.

What happens if I withdraw from my 401k early?

Withdrawing before age 59½ generally triggers a 10% early withdrawal penalty on top of income taxes. Certain hardship exceptions exist. Early withdrawal is costly. A 401k estimator will show you how much an early withdrawal reduces your retirement projection.

Conclusion:

Retirement is not something that just happens to you. It is something you build one contribution at a time. A 401k calculator is the most powerful tool to make that building intentional and measurable. You now know how it works, what inputs matter, what limits apply in 2025 and 2026, and what mistakes to avoid. The next step is simple: run your numbers. Try the calculator, adjust your contribution rate, and see what happens if you start today versus a year from now. Small changes now create differences later. Your future self will thank you for the 5 minutes you spend today.

Run your numbers in our 401 (k) calculator today. A good 401k calculator shows you exactly where you stand and what changes you need to make right now.