What Is a Good Credit Score to Buy a Car With No Down Payment?

If you want to know what credit score is needed to buy a car with no payment, I will tell you. You need to understand the credit score ranges. These ranges are important to get approved. You want to buy a car. So learning about interest rates is also helpful. It helps to know the data on interest rates. Some strategies work. Proven strategies can help you get approved. These strategies are useful when you apply them. You want to drive away without putting a single dollar down. The question you are probably asking now is what is a good credit score to buy a car with no down payment? The answer matters because it will affect how much that car will ultimately cost you over time.

This guide explains the exact credit score ranges lenders use. It also covers the interest rates you can expect at each level. It shares steps you can take today to improve your situation. These numbers show that most lenders give terms to car buyers with good finances. A credit score is important. A good credit score can help you get better loan terms. Not everyone with a credit score is left out, though.

Your credit score is shaped by five factors:

- Payment history, which is whether you pay bills on time

- Amounts owed, which is your credit utilization ratio

- Length of credit history, which is how long you have maintained accounts

- Credit mix, which is the variety of credit types you hold

- New credit, which includes hard inquiries and new accounts

What Is a Good Credit Score to Buy a Car With No Down Payment?

| FICO Score | Tier | Zero-Down Odds | Avg APR (New) | Avg APR (Used) |

| 300–500 | Deep Subprime | Very Low | ~15.84% | ~21.60% |

| 501–600 | Subprime | Limited | ~13.34% | ~19.00% |

| 601–660 | Near-Prime | Possible | ~9.50% | ~14.11% |

| 661–780 | Prime | Good | ~6.85% | ~9.70% |

| 781–850 | Super-Prime | Excellent | ~5.25% | ~7.80% |

Here is how lenders usually group credit scores for car loans, along with the chances of getting approved for a loan with no payment, and current interest rate information from Experian for the first three quarters of 2026:

FICO score: 300–500, Tier: Deep Subprime, Zero-Down Odds: Very Low, Average interest rate for new cars: about 15.84 percent, Average interest rate for used cars: about 21.60 percent

FICO score: 501–600 Tier: Subprime Zero-Down Odds: Limited, Average interest rate for new cars: about 13.34 percent Average interest rate for used cars: about 19.00 percent

FICO score: 601–660 Tier: Near-Prime Zero-Down Odds: Possible Average interest rate for new cars: about 9.50 percent Average interest rate for used cars: about 14.11 percent

FICO score: 661–780 Tier: Prime Zero-Down Odds: Good Average interest rate for new cars: about 6.85 percent Average interest rate for used cars: about 9.70 percent

FICO score: 781–850 Tier: Super-Prime Zero-Down Odds: Very Good, Average interest rate for new cars: about 5.25 percent Average interest rate for used cars: about 7.80 percent

If you have a Deep Subprime credit score, which is between 300 and 500, it is very hard to get a car loan with no down payment. Lenders think people with Deep Subprime credit scores are less likely to pay back the loan. So they usually want a down payment before they say yes to the loan. If your FICO score is in this range, you should focus on fixing your credit before you try to get a car loan.

If you have a Subprime credit score, which is between 501 and 600, it is also hard to get a car loan with no payment

Lenders that do offer credit to people with credit scores usually want a co-signer, proof that you earn a steady income, or a trade-in.

This is to reduce the risk they’re taking.

Interest rates for credit scores are also much higher.

This means you’ll pay thousands of dollars more for the car.

Near-Prime credit scores, which are between 601 and 660, make it possible to get zero-down financing. Some lenders and many credit unions will consider zero-down financing for car buyers in the prime range, particularly if other factors are in good standing. The interest rates are still elevated. Workable deals are achievable.

Prime credit scores, which are between 661 and 780, are widely considered good to good for car financing purposes. Most mainstream lenders will offer zero-down financing to car buyers. Interest rates become competitive. Your monthly payment will reflect a much more favorable structure.

Super-Prime credit scores, which are between 781 and 850, are the standard. Car buyers in the prime range qualify for the best available rates, the most flexible loan terms, and near-universal approval for no-down-payment deals. If your credit score is in this tier, you are in a position to negotiate.

Why No Down Payment Makes Lenders More Cautious:

When a car buyer puts money down, the lender’s risk decreases immediately. A down payment means the loan starts with built-in equity. Without a payment, you are financing 100% of the car’s purchase price, plus taxes and fees. Cars depreciate rapidly, which creates a scenario where you owe more than the car is worth. Lenders take on more risk in this structure, which is why credit score thresholds for zero-down deals are higher than for standard financed purchases.

What Lenders Look at Beyond Your Credit Score:

Lenders look at more than your credit score. They check things about you. This includes how much debt you have compared to your income. If you have a stable job and income, the loan amount is compared to the car’s value, and how old and what type of vehicle you want. To figure out your debt-to-income ratio. They divide your debt payments by your total monthly income before taxes. If this ratio is below 36%, you are considered to have a debt-to-income ratio. Even if your credit score is not perfect, some lenders may give you terms if you have a high income compared to your debt. If you have had a job for two or more years and have an income that can be verified, you are seen as less of a risk than someone who has a history of irregular employment. The loan-to-value ratio is how much you borrow compared to the car’s value. If you do not put any money down, this ratio is 100% or more. Lenders like loan-to-value ratios. This is why trading in your car can make it more likely that you will be approved for a loan. New cars with mileage hold their value better. This makes it less risky for lenders to give you a loan. Some lenders will only give zero-down financing for cars that are below a certain age or have low mileage.

How Credit Score Affects Your Interest Rate: A Real-World Example

Consider two car buyers who each want to finance a $30,000 used car over 60 months with no payment.

| Factor | Borrower A (760 Score) | Borrower B (580 Score) |

| Loan Amount | $30,000 | $30,000 |

| APR | ~6.85% | ~13.34% |

| Monthly Payment | ~$591 | ~$684 |

| Total Interest Paid | ~$5,460 | ~$11,040 |

| Extra Cost vs. A | — | +$5,580 |

How to Improve Your Credit Score Before Buying a Car

If your credit score is not yet where you need it to be

The way they decide who gets a loan from BNP Paribas and Credit Agricole in France is a little different from how it works in North America. But the main idea is the same for car buyers in France: you need to show BNP Paribas and Credit Agricole that you can pay back the loan on time. You also need to show them that you do not already have a lot of debt from loans.

| Strategy | Why It Works |

| Pay Bills On Time | Payment history is 35% of your FICO score. Even one missed payment can drop your score significantly. |

| Reduce Credit Card Balances | Aim to keep your credit utilization ratio below 30%. Lower is better. |

| Dispute Credit Report Errors | Check your reports via AnnualCreditReport.com. Errors are common, and correcting them can boost your score quickly. |

| Avoid New Credit Applications | Each hard inquiry temporarily lowers your score. Minimize applications in the months before car shopping. |

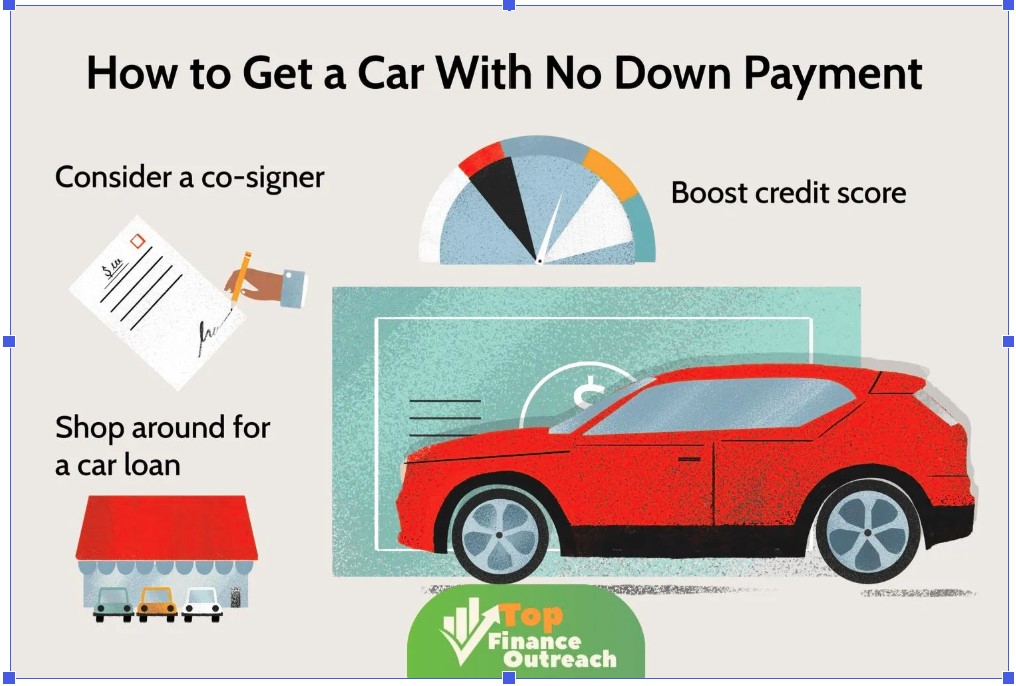

| Add a Co-Signer | A creditworthy co-signer can unlock better loan terms even if your own score is in the subprime range. |

| Consider a Trade-In | A trade-in reduces the loan-to-value (LTV) ratio, lowering lender risk even without a cash down payment. |

Lender Types and Which May Best Fit Your Situation

Not all lenders are the same. Finding the lender for your situation can make a big difference:

Credit Unions: These are kinds of banks that are owned by their members. They are not trying to make a profit, so they can be more flexible than banks. If you are already a part of a credit union or if you can join one, you should try to get a loan from them. This is especially true if your credit score is not perfect. Credit unions are an option.

Banks and Traditional Lenders: Big banks can give you interest rates if your credit score is good. If your score is 661 or higher, you should try to get pre-approved for a loan from a bank before you go to a car dealership. This will give you an idea of how much money you can borrow and what you will pay each month. Banks and lenders are a choice.

Dealership Financing: When you buy a car from a dealership, they can help you get a loan from lenders. This can be an option if you do not have credit. However, the dealership might charge you a higher interest rate than you would get from a bank or credit union. Always compare loan offers to make sure you are getting the deal. Check with dealership financing.

Subprime Auto Lenders: These lenders give loans to people who do not have credit. However, they charge interest rates, and the loan terms are not as good. If you have to use one of these lenders, try to refinance your loan after a year or so, when your credit score has improved. Subprime auto lenders are an option.

Frequently Asked Questions

Is a credit union better than a bank for a car loan?

Sometimes, yes. Credit unions often have lower interest rates and are more flexible than banks. They are an option to consider, especially if your credit score is not perfect.

Know Your Credit Score Before You Buy a Car

If you want to buy a car with no payment, you should know what your credit score is. A score of 661 is good. A score of 720 or higher is even better. Your credit score is not fixed. You can improve it over time by making financial decisions. Before you start looking for a car, you should check your credit report, fix any mistakes, and compare loan offers from lenders. This can save you a lot of money in the long run.

Conclusion:

For buyers in the United States, Canada, and France, the basics are the same: understand your credit profile, know what lenders are looking for, and try to be a low-risk borrower. Buying a car with no down payment is possible, but your credit score plays a major role in determining your approval and the cost of your loan. While some lenders may work with lower scores, a credit score of 661 or higher significantly improves your chances of qualifying for zero-down financing with reasonable interest rates. The closer you are to the prime or super-prime range (700+), the better your terms, flexibility, and overall savings will be.