Mortgage Interest Tax Deduction: How To Claim It In 2026

When you apply for a home loan, your lender will give you an interest rate. The amount you pay each month exceeds the loan amount and interest. You also have to pay property taxes, homeowners’ insurance, and private Mortgage Interest Tax Deduction insurance. A Mortgage Interest Tax Deduction helps you understand what you will really pay. This guide explains how these calculators work and what costs they include. We will look at how taxes on mortgages are different in the United States, Canada, and France.

What Is A Mortgage Calculator With Taxes?

Mortgage Interest Tax Deduction Calculator

Estimate your annual tax savings on mortgage interest — 2026

Loan Details

Your Tax Deduction Results

Loan Amount

$320,000

Annual Interest Paid

$20,480

Monthly Payment

$2,023

Deductible Interest

$20,480

Tax Savings This Year

$4,506

Monthly Tax Savings

$375

IRS Deduction Limit Check (2026)

IRS Mortgage Limit

$750,000

Deduction Status

✓ Fully Deductible

* The IRS allows mortgage interest deduction on loans up to $750,000 for homes purchased after Dec 15, 2017. Married filing separately limit is $375,000. This calculator is for estimation purposes only — consult a tax professional for advice.

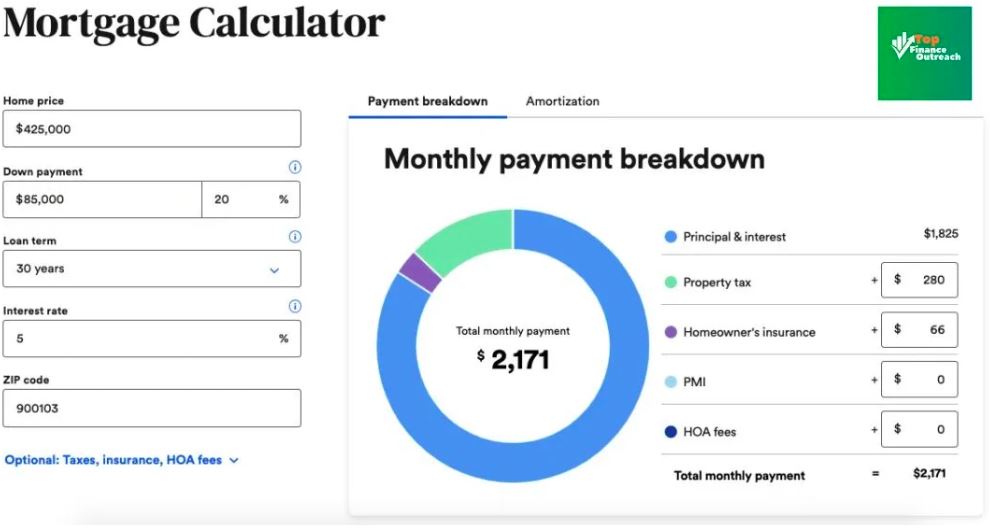

It is important to understand the difference between a calculator and a full PITI calculator so you can budget accurately. If you only look at the loan amount and interest, you might underestimate your costs by 20% to 30%. This can cause problems after you buy the house.

The home mortgage interest deduction has been a cornerstone of the US tax code for decades, see the complete legal definition here, helping millions of homeowners reduce their annual tax burden.

The Parts Of A PITI Mortgage Estimate Are:

- Principal: The part of each payment that reduces your loan balance.

- Interest: The cost of borrowing money from your lender.

- Property Taxes: Taxes on your property that you pay to your government.

- Homeowners Insurance: Insurance that protects your property against damage or loss.

- Private Mortgage Interest Tax Deduction: Insurance that you need if you put down less than 20% of the purchase price.

Homeowners Association Fees: fees for properties in a homeowners association.

Many lenders collect taxes and insurance through an escrow account. This means you pay a portion of your taxes and insurance each month with your loan payment. The lender then pays these funds to the government and your insurance company.

How Property Taxes Work In The United States:

In the United States, property taxes are set by governments like counties or cities. There is no rate. The average property tax rate is around 1.1% of the property’s value each year. However, rates vary significantly by location. When you use a Mortgage Interest Tax Deduction with taxes, it will apply a default tax rate based on averages. You should enter the specific rate for your area to get an accurate estimate. Property investors can use our Negative Gearing Calculator to calculate potential tax benefits alongside their mortgage interest deductions

To calculate property taxes, you multiply the property’s value by the tax rate. Most areas assess property at 80% to 100% of its market value. Then they apply a tax rate to this value.

For example, if a house is worth $350,000 and the tax rate is 1.2%, the annual property tax would be $4,200 or $350 per month.

You can also deduct the Mortgage Interest Tax Deduction from your income taxes. This can reduce your income. However, there are limits to how much you can deduct.

CMHC Insurance Premiums (2024)

| Loan-to-Value Ratio | CMHC Premium Rate |

| 80.01% – 85% | 2.80% of the loan amount |

| 85.01% – 90% | 3.10% of the loan amount |

| 90.01% – 95% | 4.00% of the loan amount |

Mortgage Taxes & Insurance in Canada:

The Canadian Mortgage Interest Tax Deduction system is different from the system. If you put down less than 20% of the purchase price, you need to get mortgage default insurance through the Canada Mortgage and Housing Corporation. This insurance is added to your loan amount. Is subject to federal taxes.

A Mortgage Interest Tax Deduction calculator for users should include a field for this insurance. For example, if you buy a $500,000 house with a 10% down payment, the loan amount is $450,000. The insurance premium would add $13,950 to the mortgage balance.

Property taxes in Canada are set by municipalities. Vary by province. You should enter your estimated tax rate into a comprehensive Canadian Mortgage Interest Tax Deduction calculator.

Mortgage Costs & Property Taxes In France:

In France, property taxes are administered locally. Are different from North American systems. There are two property taxes: the Taxe Foncière and the Taxe d’Habitation. The Taxe Foncière is a tax on property ownership, and the Taxe d’Habitation is a tax on second homes.

When using a Mortgage Interest Tax Deduction calculator for property, you should budget for the Taxe Foncière separately from your monthly mortgage payment. French property taxes are billed annually. Paid directly by the homeowner.

You should also consider registration duties and notary fees when buying a property in France. These one-time costs are around 5% to 6% of the purchase price for existing properties and 2% for properties.

How To Use A Mortgage Calculator With Taxes Effectively:

To get an estimate, you need to enter the right data into the calculator. Here’s how:

Step 1. Gather your input variables, home purchase price, or appraised value.

- You should also consider costs like homeowners’ insurance and private Mortgage Interest Tax Deduction insurance. By following these steps, you can use a mortgage calculator with taxes to get an idea of your monthly housing costs.

- Down payment amount, which is the amount of money you pay upfront when you buy a house, can be a dollar figure or a percentage of the cost.

- The loan term is how long you have to pay back the loan. It can be 15 years, 20 years or 30 years or 25 years in Canada.

- The interest rate is the percentage of the loan that you pay as interest. You should get a rate quote from at least three lenders to compare.

- The annual property tax rate is the amount of money you pay each year in taxes on your house. It varies depending on where you live.

- The annual homeowners’ insurance premium is the amount of money you pay each year to insure your house. It is usually around 0.5% to 1% of the value of your house in the USA.

- HOA monthly fees are the amount of money you pay each month to your homeowners association if you have one.

- PMI rate is the amount of money you pay each month for Mortgage Interest Tax Deduction insurance if you put down less than 20% as a down payment in the USA.

Step 2. Understand What the Calculator Returns:

A good Mortgage Interest Tax Deduction calculator with taxes will break down your payment into individual parts so you can see exactly how much you are paying for each thing. A lender has to give you a document called a Loan Estimate, which shows all the costs of the loan within three business days of getting your application. This document should have the costs as calculated by the calculator.

Step 3. Run Multiple Scenarios

You should use the calculator to see how different things affect your payment. For example, if you put down 20% of 10%, you might not have to pay PMI, which can save you around $100 to $250 per month on a $300,000 loan. In Canada, if you put down 20%, you do not have to pay CMHC insurance, which can save you a lot of money over the life of the loan.

Step 4. Apply the 28/36 Rule

A lot of planners say you should not spend more than 28% of your monthly income on housing costs and not more than 36% on all debt payments. A Mortgage Interest Tax Deduction calculator with taxes can help you figure out how much house you can afford based on this rule. You can put in your income. The calculator will tell you the maximum purchase price you can afford. Managing multiple financial commitments like tuition and mortgage? Our College Finance Calculator helps you balance education costs while maximizing your mortgage interest tax deduction

Common Mistakes to Avoid

One mistake people make is using the national average tax rate instead of the rate for their specific area. Property tax rates can be very different depending on where you live. For example, in Newark, New Jersey, the property tax rate is over 3%. In Honolulu, Hawaii it is less than 0.3%. If you use the tax rate, your estimate will be wrong.

Another mistake is not including homeowners’ insurance in your calculation. Insurance costs can be higher in areas that’re prone to natural disasters.

You should also not forget to account for inflation, which can increase your property taxes and insurance costs over time.

Bi-Weekly Payments & Accelerated Payoff:

Some people get confused between the assessed value of their house and the market value. The assessed value is what the county uses to calculate your property taxes. It might be different from the market value.

A lot of Mortgage Interest Tax Deduction calculators with taxes can also show you how making bi-weekly payments can affect your loan. If you make weekly payments, you make 26 half-payments per year, which is like making 13 full monthly payments. This can save you a lot of money in interest over the life of the loan. Can even shorten the loan term by four to six years. If you are planning your retirement alongside your mortgage, use our 401 (k) Calculator to see how much you need to save alongside your mortgage interest deductions.

In Canada, making accelerated bi-weekly payments is a strategy because it can save you a lot of money on your Mortgage Interest Tax Deduction.

This article is about Mortgage Interest Tax Deduction calculators with taxes. It covers a lot of related topics, including PITIMortgage Interest Tax Deduction calculators, property tax mortgage estimates, and mortgage payment breakdowns.

(FAQ)

What is included in a mortgage calculator with taxes?

A Mortgage Interest Tax Deduction with taxes includes the principal, interest, property taxes, homeowners’ insurance, and PMI. Some calculators also include HOA fees, closing costs, and other expenses.

How accurate are online mortgage calculators?

Online calculators are pretty accurate if you put in the right information. You have to make sure you use the right property tax rate for your area, and you should always get a formal Loan Estimate from your lender before making any decisions.

Is PMI the same as mortgage insurance in Canada?

No PMI and Mortgage Interest Tax Deduction in Canada is not the thing. In the USA, PMI is an insurance policy that you buy to protect the lender. In Canada, mortgage insurance is provided by the government. It is usually added to the loan amount instead of being paid monthly.

Do French mortgage payments include property taxes?

No French Mortgage Interest Tax Deduction payments do not include property taxes. In France, property taxes are billed annually. Paid directly by the homeowner.

How does the mortgage stress test affect my calculator results in Canada?

The mortgage stress test in Canada requires lenders to qualify borrowers at a higher interest rate than the actual rate. When you use a Mortgage Interest Tax Deduction calculator, you should use the stress-test qualifying rate to get an estimate of how much you can afford.

Can I deduct property taxes on my mortgage in the USA?

Yes, you can deduct property taxes on your Mortgage Interest Tax Deduction in the USA if you itemize your deductions on your tax return. But there is a limit on how much you can deduct, so you should talk to a tax professional to see if it makes sense for you.

Conclusion:

A Mortgage Interest Tax Deduction calculator with taxes is an important tool for people who are buying a house. It helps you figure out how much your monthly payment will be, and it includes things like property taxes, homeowners’ insurance, and PMI. You have to make sure you put in the information, like the property tax rate for your area, to get an accurate estimate. Whether you are buying a house in the USA, Canada, or France, a Mortgage Interest Tax Deduction calculator with taxes can help you make a decision. You should always talk to a mortgage broker and a qualified tax advisor to make sure you understand all the costs and rules.